Capital Budgeting: What Is It?

In capital budgeting, projects that improve a business are chosen. Almost everything, including the acquisition of land or the purchase of fixed assets like a new truck or machinery, can be included in the capital budgeting process. There are several approaches to capital budgeting, and businesses employ multiple criteria to monitor the performance of proposed projects.

KEY LESSONS

Investors estimate the worth of new investment projects using capital budgeting.

Payback period (PB), internal rate of return (IRR), and net present value (NPV) are the three methods of project selection that are most frequently used (NPV).

How long it would take a business to generate enough cash flow to recoup the initial investment is determined by the payback period.

The predicted return on a project is measured by its internal rate of return; if it exceeds the cost of capital, the project is good.

The net present value, which compares a project's profitability to alternatives, is likely the most useful of the three techniques.

Knowledge of capital budgeting

Companies frequently coordinate efforts across divisions and rely on financial leadership to assist with the creation of yearly or long-term budgets. These budgets, which frequently include operational details, show how the company's revenue and expenses will develop over the course of the following 12 months. Capital budgeting, however, is another element of this financial strategy. The long-term financial strategy for greater financial expenditures is capital budgeting.

Many of the same core techniques used in other budgeting methods are also used in capital budgeting. However, capital budgeting faces a number of particular difficulties. First off, capital budgets are frequently only cost centers; they require funding from an outside source, such as money from another department, because no revenue is generated during the project. Second, there are greater risks, ambiguities, and potential problems because capital budgets are long-term in nature.

For long-term projects, capital budgeting is frequently created, then revised as the project or effort progresses. As a project advances, businesses frequently reprojection their capital budget. A capital budget is crucial for anticipating big cash inflows that, once they begin, shouldn't be stopped unless the business is ready to bear significant potential project delay costs or losses.

Why Is Capital Budgeting Necessary for Business?

Budgeting for capital projects is crucial because it fosters accountability and measurement. Any company that wants to commit resources to a venture without fully comprehending the dangers and potential rewards will be viewed as irresponsible by its owners or shareholders. Additionally, if a company has a mechanism to assess the success of its investment choices, it is unlikely that it would survive in the cutthroat commercial environment.

Companies frequently find themselves in a situation where their funding is constrained and their options are limited. Decisions about how to divide up labor hours, capital, and resources are typically up to management. As it describes the goals for a project, capital budgeting is crucial to this process. These goals can be compared to those of other initiatives to see whether one or ones are best.

Businesses—aside from nonprofits—are in operation to make money. Businesses may quantify the long-term economic and financial profitability of any investment project through the capital budgeting process. While predicting sales for the upcoming year may be simpler for a business, it may be more challenging to predict how a five-year, $1 billion manufacturing headquarters refurbishment would turn out. Therefore, firms require capital budgeting to evaluate risks, make future plans, and anticipate difficulties before they arise.

Approaches to Capital Budgeting

There is no one best way for capital budgeting; in fact, businesses can find it useful to create a single capital budget utilizing a combination of the many approaches covered below. By doing so, the business can spot gaps in one study or take into account implications across other approaches that it might not have otherwise considered.

Analysis of Discounted Cash Flows

Companies frequently utilize discounted cash flow methodologies to evaluate both the timing and implications of the dollar because a capital budget will frequently span multiple periods and maybe many years. Currency values frequently decline over time. A fundamental idea in economics dealing with inflation is that money now is worth more than money tomorrow because money today can be used to make money tomorrow.

The inflows and outflows of a project are included in discounted cash flow as well. Companies frequently have to make an initial financial investment for a project (a one-time outflow). Other times, there might be a string of outflows that are used to pay for ongoing projects. Companies may aim to determine a target discount rate or a certain net cash flow amount at the conclusion of a project in either scenario.

Payback Evaluation

Payback techniques of capital budgeting make plans around the timing of when specific benchmarks are reached rather than just focusing on dollars and returns. Some businesses seek to monitor when they become profitable (or has paid for itself). Others are more focused on when a capital project will start to generate a certain amount of profit.

Capital budgeting necessitates the requirement for meticulous cash flow forecasts for payback strategies. This strategy necessitates a little more timing attention because any variation in an estimate from one year to the next may significantly affect when a company may meet a payback metric. If a business wants to combine capital budget approaches, it can also combine the payback method with the discounted cash flow analysis method.

Utilization Analysis

Throughput analysis-based solutions for capital planning represent a vastly different approach. Throughput methods examine revenue and expenditures across the board, not just for particular initiatives. Operational or non-capital budgeting can also use throughput analysis through cost accounting.

Throughput methods involve deducting variable costs from a company's revenue. By using this technique, it is possible to determine how much of each sale's profit can be attributed to fixed costs. Any throughput is retained by the firm as equity once all fixed costs have been covered by the business.

Companies could aim to have a target quantity of capital available after variable costs in addition to making a specific amount of profit. The management may establish a target for how much the capital budget projects must provide back to operations, and these monies can be used to pay for operational costs.

Budgeting for Capital: Metrics

Finding out whether or not a project will be profitable is one of a company's first jobs when faced with a capital budgeting choice. The most popular strategies for choosing projects are the payback period (PB), internal rate of return (IRR), and net present value (NPV) methodologies.

Although the three measures should all point to the same decision in an ideal capital budgeting strategy, these methods frequently lead to inconsistent outcomes. There will be a preference for one strategy over another based on management preferences and selection criteria. Even Nevertheless, these generally accepted systems of valuation have certain shared benefits and drawbacks.

Payment Period

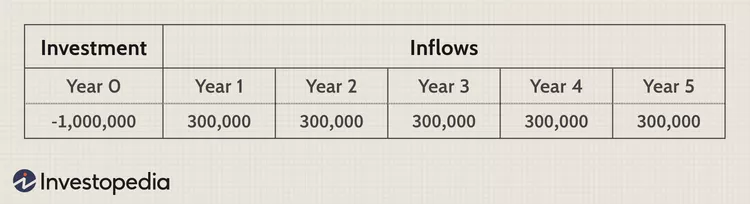

The payback period determines how long it will take to make back the initial investment. The PB shows how many years are needed for the cash inflows to equal the one million dollar outflow, for instance, if a capital budgeting project calls for a $1 million beginning cash outlay. A brief PB term is preferable since it suggests that the project would "pay for itself" more quickly.

The PB term in the next case would be three and a third years, or three years and four months.

When liquidity is a key concern, payback periods are frequently used. A corporation could only be able to take on one significant project at a time if it has a certain amount of funding. As a result, management will put a lot of effort into getting their initial investment back in order to move forward with new projects.

Once the cash flow estimates have been produced, another significant benefit of employing the PB is that calculations are straightforward.

The PB measure has limitations when used to make capital budgeting decisions. First off, the time value of money is not taken into account by the payback period (TVM). A statistic that equally emphasizes payments made in years one and two is provided by computing the PB.

Such a mistake goes against a fundamental tenet of finance. Fortunately, this issue is easily resolved by using a discounted payback period model. Basically, the discounted PB period takes TVM into account and lets you calculate how long it will take to repay your investment on a discounted cash flow basis.

Another disadvantage is that both payback periods and discounted payback periods neglect cash flows like salvage value that happen toward the conclusion of a project's life. As a result, the PB is not a precise indicator of profitability.

https://www.investopedia.com/terms/c/capital-project.asp

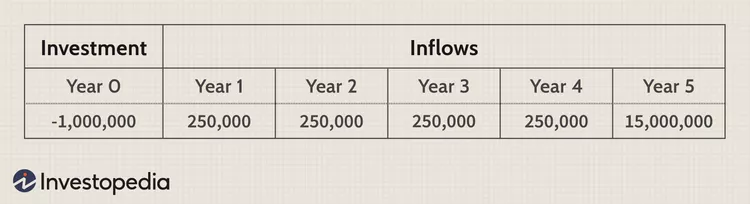

The following example's PB period is four years, which is worse than the previous example's, but for the purposes of this statistic, the significant $15,000,000 cash influx that occurs in year five is disregarded.

The payback technique has additional limitations, such as the potential requirement for monetary investments at various project stages. Additionally, the asset's lifespan should be taken into account. There could not be enough time to make money off the project if the asset's life does not last very long after the payback period.

The payback time is typically regarded as the least pertinent valuation approach because it does not take into account the extra value of a capital budgeting choice. However, PB periods are crucial if liquidity is an important factor.

Rate of Return Internal

The discount rate that would result in a net present value of zero is known as the internal rate of return (or projected return on a project). The benchmark for IRR calculations is the actual rate used by the firm to discount after-tax cash flows since the NPV of a project is inversely connected with the discount rate—if the discount rate increases, future cash flows become more uncertain and therefore lose value.

When the IRR exceeds the weighted average cost of capital, it is assumed that the capital project will be profitable, and the opposite is also true.

The following is the IRR rule:

IRR > Capital Expenditures = Project Acceptance

Cost of Capital x IRR = Project Reject

The IRR in the case below is 15%. The project should be approved if the company's actual discount rate, which is what they use for discounted cash flow models, is less than 15%.

The internal rate of return can be used as a decision-making tool primarily because it offers a benchmark value for each project that can be evaluated in relation to a company's capital structure. The IRR typically yields decisions that are similar to those produced by net present value models and enables businesses to assess projects based on returns on capital invested.

Although it is simple to calculate the IRR using a financial calculator or programmed, there are certain drawbacks to doing so. Similar to the PB technique, the IRR just provides a benchmark figure for which projects should be approved based on the firm's cost of capital, not a true sense of the value that a project will provide to a firm.

⛳️ Estos son los MEJORES CURSOS sobre FINANZAS GRATIS para empezar a TOPE este 2023

— Héctor Mohedano (@HMohedano_) January 7, 2023

• Fixed-income securities

• Asset valuation

• Capital budgeting

• Common stocks

• Portfolio selection

• An introduction to derivatives and options

Y mucho más… 👇🏼 pic.twitter.com/KeYq7BQRrI

Managers could be able to identify that projects A and B are both advantageous to the firm, but they would not be able to decide which is better if only one can be approved because the internal rate of return does not allow for an appropriate comparison of mutually exclusive initiatives.

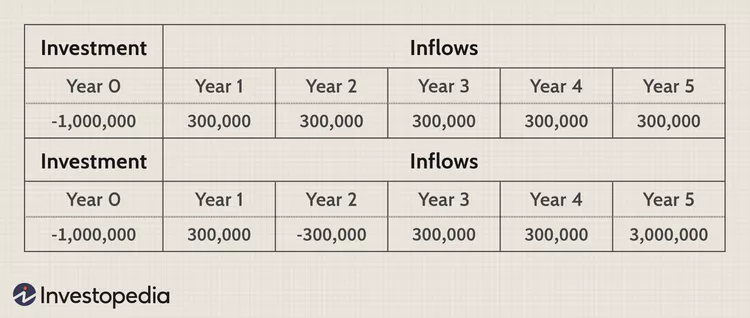

When a project's cash flow streams are irregular, which means that there are further cash outflows after the first investment, this poses another problem with the use of IRR analysis. Since many projects have future capital expenditures for maintenance and repairs, unusual cash flows are frequent in capital budgeting. In this case, there might not be any internal rates of return or there might be several. There are two IRRs in the case below: 12.7% and 787.3%.

When evaluating individual capital budgeting projects, not those that are mutually exclusive, the IRR is a relevant valuation metric. Although it offers a superior valuation option to the PB technique, it fails to meet a number of important criteria.

Value Net Present

The most understandable and precise method for valuing issues with capital budgeting is the net present value approach. Using the weighted average cost of capital to discount the after-tax cash flows, managers can assess the profitability of a project. Additionally, unlike the IRR technique, NPVs show the exact profitability of a project in relation to alternatives.

According to the NPV rule, all projects with a positive net present value should be approved, while those with a negative net present value should be turned down. If there aren't enough funds to start all positive NPV projects, the ones with the highest discounted values should be approved.

Project A and project B in the two cases below have respective NPVs of $137,236 and $1,317,856 under the assumption that the discount rate is 10%. These findings indicate that both capital budgeting initiatives would raise the firm's worth, however project B is preferable if the company currently has only $1 million to invest.

The NPV technique has a number of significant benefits, including its general applicability and the fact that it gives a clear indication of increased profitability. It enables the comparison of numerous projects that are mutually exclusive at once, and even if the discount rate is liable to change, a sensitivity study of the NPV often identifies any sizable potential future concerns.

Although the profitability index (PI), a statistic derived from discounted cash flow calculations, can readily address this worry, the NPV technique is vulnerable to reasonable critiques that the value-added figure does not take into account the entire scope of the project.

The profitability index is determined by dividing the initial investment by the present value of future cash flows. If the PI is more than 1, the NPV is positive; if it is lower than 1, the NPV is negative. Despite being challenging to compute, weighted average cost of capital (WACC) is a reliable indicator of investment quality.

What Kinds of Budgets Are Typically Used?

It is possible to prepare incremental, activity-based, value-based, or zero-based budgets. While some types, such as zero-based budgets, start a budget from scratch, incremental or activity-based budgets may take inspiration from a budget from a previous year to have a baseline. Any of the aforementioned techniques can be used to create a capital budget, although zero-based budgets are best for brand-new projects.

How Differ From Operational Budgets Are Capital Budgets?

Budgets for capital expenditures frequently cover several years and are more long-term oriented. Operational budgets, meanwhile, are frequently created for one-year periods that are determined by revenue and expenses. Operational budgets keep track of a company's daily operations, whereas capital budgets frequently involve other types of initiatives like redevelopments or investments.

Do Businesses Need to Create Capital Budgets?

Not necessarily; capital budgets are internal planning tools, just like all other budgets. These reports are primarily intended to support management's strategic decision-making and are not required to be made public. Even though they are not essential, capital budgets play a crucial role in planning and a company's long-term performance.

The conclusion

A capital budget is a long-term strategy that details the financial requirements of a big acquisition, development, or investment. An analysis of the capital budget is necessary to determine whether the long-term project will be profitable, as opposed to an operational budget that records revenue and expenses. NPV, IRR, and payback periods are frequently used to examine capital budgets to ensure that the return fulfils management expectations.