What Are Capital Expenditures (CapEx)?

The money that is spent by a corporation to purchase, improve, and maintain its tangible assets, like as land, plants, buildings, machinery, or other types of technology, is referred to as capital expenditures, or CapEx for short. These expenditures are also known by their acronym. The term "CapEx" is commonly used to refer to these expenditures of money. The launch of brand-new initiatives or investments in brand-new businesses is one of the most common uses of a company's capital expenditures. Activities such as repairing a roof (which, if done properly, can increase the usable life of the roof), purchasing a piece of machinery, or constructing a new factory are all examples of activities that fall under the category of capital expenditures and can be considered forms of investment in fixed assets. Other examples of capital expenditures include: Companies make financial investments of this kind for one of two reasons: either to broaden the scope of their operations or to add some future economic value to the operations that they are currently carrying out.

The section of a cash flow statement that is titled "cash flow from investment activities" is where a company's capital expenditures will be displayed if the cash flow statement is prepared for an organisation. A significant percentage of businesses will refer to purchases of property, plant, and equipment as capital expenditures (also known as CapEx). Other names for capital expenditures include capital spending and acquisition expense (PP&E). An analyst or investor looking over the financial accounts of a company can come across any one of these terms at some point.

The information that is seen on the balance sheet and income statement of a firm can also be utilised to compute the total amount of capital expenditures made by that company. You can find the amount that has been recorded as the depreciation expense for the current period by searching in the relevant location in the income statement. This is the amount that has been reported. Find the line-item balance that corresponds to the current period on the balance sheet, and look for it under the heading that reads "property, plant, and equipment."

Das ist offensichtlich der Grund hier.

— Poorly Informed Novice (@StupidBaby20) February 21, 2023

In der Rechnungslegung heißt das CapEx, und man investiert es nur in dem Maße, wie man es über die nächsten Jahrzehnte wirklich braucht.

Daher will KMW Planungssicherheit für Produktionsvolumina.https://t.co/wt5dppbYy3

The change in the PP&E balance for the company can be determined by first obtaining the PP&E balance from the previous period for the company, and then by taking the difference between the PP&E balance from the previous period and the PP&E balance from the current period. This will give you the change in the PP&E balance for the company. To begin, take the depreciation costs from the previous period and add them to the fluctuation in the PP&E expense. Having this information will bring you one step closer to determining the current-period capital expenditures for the company.

KEY TAKEAWAYS

The private ownership of the means of production, particularly in the industrial sector, and the payment of labour solely in the form of wages rather than any other form of compensation distinguish capitalism as a distinct form of economic organisation. Capitalism is most commonly associated with the era of industrialization. Capitalism can be differentiated from other types of economic organisation based on these two distinguishing traits.

Due to the fact that these rights encourage financial investments in productive capital and the efficient use of that capital, the protection of private property rights is absolutely necessary to the smooth operation of capitalism. This is because these rights encourage financial investments.

It is possible to trace the historical roots of capitalism all the way back to Europe, where it developed from prior forms of economic organisation such as mercantilism and feudalism. The historical origins of capitalism may be traced all the way back to Europe. The historical roots of capitalism can be traced back to the year 1500 in Europe. These roots were laid in Europe. It is generally believed that capitalism was the driving force behind the enormous improvements made in industrialization and the broad availability of consumer products on the mass market. [Citation needed] [Citation needed] [Citation needed] [Citation needed] [Citation needed

Pure capitalism can be contrasted with pure socialism, which is an economic system in which all means of production are owned either collectively or by the state, as well as mixed economies. Pure socialism is an economic system in which all means of production are owned either collectively or by the state. An economic system is considered to be in its purest form to be socialism when all of the means of production are owned either collectively or by the state. If all of the means of production are held by the same entity, whether it be a collective entity or the state, then an economic system is regarded to be socialist in its most fundamental form (which lie on a continuum between pure capitalism and pure socialism).

Because of the pressure from businesses seeking favourable government intervention and the motivation for governments to meddle in the market, the practical implementation of capitalism in the real world often involves some degree of the so-called "crony capitalism." This is because of the pressure from businesses seeking favourable government intervention. The pressure exerted by businesses who were looking for favourable government intervention led to the naming of this particular style of capitalism. This is because governments are given incentives to interfere with the natural operations of the economy, which has led to the current situation.

There are Many Variations Regarding the Topic of Capital Expenditures

A company's assets can deliver it a varied range of long-term value in a variety of forms. The company stands to benefit from the contribution of this value. As a direct result of this, the term "capital expenditure" can be used to refer to a wide variety of different kinds of purchases. This is because of the direct connection between the two.

Buildings have the capacity to perform a wide variety of functions, including but not limited to the provision of office space, the manufacturing of items, the storage of inventory, and many other functions as well.

The land carries with it the possibility of undergoing further development at some point in the future. When land is purposely held for the aim of using it as a speculative long-term investment, the typical accounting practise may diverge from how land is handled in these situations.

The process of making things, as well as the process of turning raw materials into finished products, are both processes that can be made easier with the assistance of a wide variety of different pieces of equipment and different types of technology.

Computers and servers can be used to provide aid to the operational parts of a firm, such as the logistics, reporting, and communication of operations, and this assistance can be made available by using the operational aspects of a company. It is feasible that, under some conditions, software may also be considered as an example of capex. This possibility exists because software is an investment.

Before the employees of the office building or the consumers of the business are able to use the interior space of the building, it must first be furnished with appropriate office equipment.

Employees have the opportunity to use company vehicles for work-related errands like picking up customers or transporting items, as well as the capability to do so. Some examples of these jobs include picking up customers or moving items.

Patents have the potential to keep their value over the long term, particularly if the right to hold an idea is materialised through the production of a product. This would ensure that the patent's value is not diminished over time.

The Thought Process That Goes Into Developing the Formula and Figuring Out Capital Expenditures

The formula for calculating capital expenditures is as follows: CapEx = (Production Plant and Equipment) - (Current Depreciation), where CapEx = Capital Expenditures

Any alterations that have been made to the property, plant, or equipment are denoted by the notation PP&E in financial documents.

The abbreviations "CapEx," "PP&E," and "CD" refer, respectively, to "capital expenditures," "personal property and equipment," and "current depreciation," respectively. Any alterations that were made to the property, plant, and equipment are denoted by the notation PP&E in the accounting records.

While determining the free cash flow to equity ratio, capital expenditures are one of the factors that are factored in throughout the calculation process (FCFE). The term "free and clear earnings," or FCFE, refers to the cash that is readily available to equity investors. Cash like this is easily accessible to equity owners. Below is a list of the components that make up the FCFE formula:

The following constitutes the formula for FCFE: The formula for FCFE is as follows: FCFE = EP s s(sCE s D) s s(s1 s DR s) s s sC s s (s1 s sDR s) s where:

The phrase "free cash flow to equity" is represented by the abbreviation "FCFE."

Earnings per share is abbreviated as EP, capital expenditures as CE, and depreciation is abbreviated as D. All of these abbreviations are used interchangeably throughout this article. The term "debt ratio" is often abbreviated as "DR."

The difference between the previous amount of net working capital and the current amount of net capital is denoted by the letter C.

The abbreviation "FCFE" stands for "free cash flow to equity." EP(CED)(1DR)C(1DR) is the formula that is used to calculate it, and FCFE is an acronym that stands for free cash flow to equity.

Earnings per share is what is meant by the abbreviation "EP."

CE = Capital Expenditures; sD = Depreciation

DR stands for "debt ratio."

The change in both the overall net capital and the net working capital is what is denoted by the letter C.

Instead, one might compute it using the method described here as an alternative:

The following constitutes the formula for FCFE: The formula for calculating FCFE is as follows: NI * NCE * C * C + N D * D R, where NI is an abbreviation for "net income."

NCE = Net CapEx

ND = New debt

DR = Debt repayment

The formula for calculating FCFE is as follows: NI + NCE plus C plus ND plus DR, where NI stands for "net income."

NCE=Net CapEx ND=New debt

DR=Debt repayment

Taking Into Account All of the Particulars

The capital expenditure (CapEx) indicator is not only used to analyse a company's investment in its fixed assets, but it is also incorporated in a range of different company analysis ratios. In addition, the indicator is used to evaluate a company's overall financial health. Also, the indicator is utilised in the process of analysing the investment made by a corporation in its mobile assets. The cash-flow-to-capital-expenditures ratio, commonly known as the CF-to-CapEx ratio, is a gauge of the ability of a corporation to buy long-term assets using cash flow from operations. Another name for this ratio is the CF-to-CapEx ratio. This ratio is also known by the name cash flow to capital expenditure ratio. As a result of the ebb and flow of the cycles of large and small capital expenditures that characterise a company's business, the ratio of an organization's operating cash flow to its capital expenditures will routinely fluctuate. This is one of the characteristics that distinguishes an organisation from another.

If the ratio is greater than one, this may indicate that the company's operations are producing the cash that is necessary to fund the acquisition of its assets. If the ratio is less than one, this may indicate that the company's operations are not producing the cash that is necessary. If the ratio is lower than one, this may suggest that the operations of the company are not creating the required amount of cash. On the other side, a low ratio may suggest that the firm is experiencing difficulties with its cash inflows and, as a result, its purchase of capital assets. This is because a low ratio indicates that the company is purchasing fewer assets. This can be deduced by looking at the ratio, which shows that it is rather low. If a company's ratio is lower than one, it may be needed to seek a loan in order to finance the purchase of capital assets. This may be the case even if the company's ratio is higher than one. Even if the corporation has a positive net worth, this can still be the situation.

Examining the Difference Between Operational and Capital Expenditures (OpEx)

It is vital to create a distinction between the costs of running the business and the costs of investing in the business (OpEx). Operational expenses are expenditures that must be made on a short-term basis in order to satisfy the constant operational costs of running a firm. These costs can be broken down into direct and indirect operating expenses. In order for a business to continue functioning normally, it is necessary to cover these expenses. When opposed to capital expenditures, operating expenses are able to be deducted in their whole from a company's taxable income in the same year that the expenses were spent. This is in contrast to the treatment of capital expenditures, which cannot be deducted in their entirety. Expenditures on capital assets are not subject to this rule.

When an expense is incurred that extends the usable life of an existing capital asset, or when an asset is a newly purchased capital asset or an investment that has a life of more than one year, an accountant will refer to this type of charge as capital expenditure. Another example of when an accountant might use this term is when an asset is a newly purchased investment that has a life of more than one year. This holds true irrespective of whether the asset in question is one that was recently acquired as part of a capital expenditure or one that is an investment with a duration of more than one year (CapEx). If, on the other hand, the expense is one that maintains the asset in the same state as it is currently in, such as a repair, then the cost is generally deducted in its entirety in the same year that the expense is spent, with the exception of situations in which the expense is one that brings the asset to a new state. One good illustration of this would be the cost of an insurance premium.

Capital Expenditure Examples

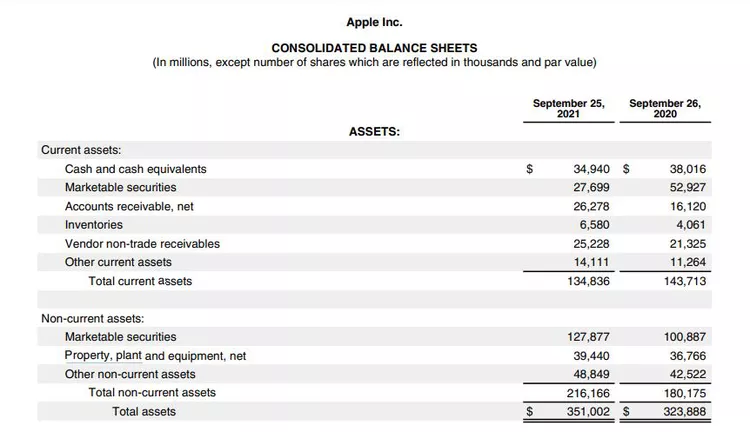

Apple Inc. disclosed in the financial files that it produced at the conclusion of its fiscal year 2021 that the total value of all of its assets amounted to 351 billion dollars. This information was included in the papers. The company stated that the value of its property, plant, and equipment totaled 39.44 billion dollars after taking into account the total amount of accumulated depreciation, despite the fact that it had recorded an asset value of 39.44 billion dollars. This was despite the fact that the company had recorded an asset value of 39.44 billion dollars.

These balances are required to be computed in this fashion in accordance with the Generally Accepted Accounting Principles (GAAP) (GAAP). The regulations, methods, and policies that must be followed when a company is obligated to account for capital expenditures often match Apple's handling of the situation below.

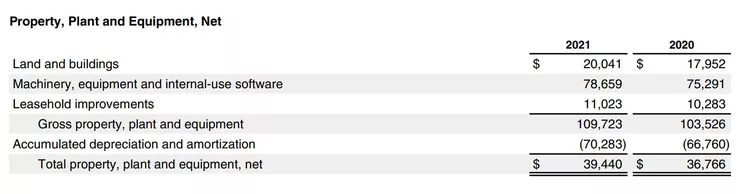

On Apple's balance sheet, the whole inventory of the company's property, plant, and equipment is consolidated onto a single line item. However, extra information on property, plant, and equipment is normally required to be provided within the notes that are attached to the financial statements. This is because the notes are an integral part of the financial statements. According to these supplementary pieces of information, Apple possesses PPE with a total gross value of $109 billion, nearly 79 billion of which is comprised of machinery, equipment, and internal-use software. With regard to this specific instance.

Also, an explanation of how the cumulative depreciation balance contributes to the lowering of the property, plant, and equipment balance can be found in the notes section. In the context of this particular example, Apple has made use of $70.3 billion of the total $109.7 billion in expenditures on capital. At the present time, the book value of this particular category of capital expenditures is 39.4 billion dollars.

'Although this is merely a thought experiment, it should be helpful in illustrating how CapEx works. Let's say that during the same fiscal year, ABC Company invested $7.46 billion in capital improvements while XYZ Corporation invested $1.25 billion in the purchase of property, plant, and equipment. Let's also say that ABC Company spent more on capital improvements than XYZ Corporation did. The cash flow from operations that ABC Company and XYZ Corporation had at the end of the fiscal year was $14.51 billion for ABC and $6.88 billion for XYZ Corporation, respectively.

The following formula can be used to calculate the ratio of CF to CapEx:

CF/CapEx is an abbreviation for "Cash Flow to Capital Expenditures." It is calculated by dividing Cash Flow from Operations by Capital Expenditures. CF/CapEx equals Cash Flow from Operations.

Cash Flow from Operations minus Capital Expenditures is the formula used to calculate CF/CapEx.

where the ratio being utilised is Cash Flow to Capital Expenditures (CF/CapEx).

The following is a breakdown of how ABC's CF-to-CapEx is calculated using this method:

$ \s1 \s4 \s. \s5 \s1

billion s$ billion s7 s. four billion six

The number of zeroes in a billion equals one zero in a one.

$7.46 Billion

$14.51 Billion =1.94

The following is XYZ's ratio of cash flow to capital expenditures:

$ \s6 \s. \s8 \s8

a billion dollars worth of s1, s2, and s5

Billion is equal to s5. Billion is equal to s9.

$1.25 Billion

$6.88 Billion =5.49

It is very important to keep in mind that this ratio is one that is specific to a certain industry, and that it should only be compared to a ratio that has been generated from another company that has requirements for CapEx that are comparable to those of the first company. Keeping these two points in mind is very important.

What Sort of Investment Does a Company Make When They Make Capital Expenditures?

The investments that a corporation makes in order to expand or maintain its business activities are what are referred to as capital expenditures, which are also abbreviated as CapEx. In contrast to operating expenses, which tend to remain essentially unchanged from one year to the next, forecasting capital expenditures can be a bit more challenging. A purchase of expensive new machinery, for instance, would be seen as a capital expenditure when made by a company because of the considerable amount of money that is invested in making the acquisition. As a direct result of this, the cost of the equipment would be gradually deducted from the total amount owed over the course of its productive life.

Is It Doable to Take a Tax Deduction for Capital Expenses?

Capital expenses are not directly tax deductible. Nonetheless, since they result in depreciation, they have the ability to decrease a company's taxes in an indirect manner. This is one of the benefits that they offer.

For instance, if a company purchases a piece of equipment for $1 million that has a useful life of 10 years, the corporation might be required to account for depreciation expenses that total $100,000 per year for those 10 years. This is because the useful life of the equipment is longer than the useful life of the equipment. Because of this depreciation, the annual pretax income of the company would decrease by $100,000, which would lead to a decrease in the amount of income tax that the company would be required to pay as a result of this situation.

How Are Operating Costs and Capital Expenditure Apart from One Another?

The major difference between operating expenses and capital expenditures is that operating expenses are those that recur on a regular and predictable basis. Capital expenditures, on the other hand, are one-time payments made to acquire assets. Rent, labour, and the cost of utilities are a few examples of expenses that fall under the category of running costs. Contrarily, expenditures on capital are likely to occur a great deal less frequently and with a great deal less constancy than operational expenses. When compared to capital expenditures, which only cut taxes through the depreciation that they cause, operating expenses can be deducted in their entirety and are reflected on the income statement. Capital expenses are not tax deductible.

What does the term "CapEx" actually stand for?

The term "capital expenditures," which refers to significant purchases that are typically capitalised on the balance sheet of a corporation rather than being expensed, is sometimes shortened to "capex." Large purchases are routinely capitalised on the balance sheet of a firm.

In What Way Does an Example of a Capital Expenditure Look Like?

It is common practise for a company to capitalise and record as capital expenditure any transaction involving the purchase of a new vehicle for the company's fleet (CapEx). After first being recorded on the company's balance sheet, the acquisition is then subject to having the cost of the vehicle written down during the duration of its useful life in order for the company to be able to recognise a profit from the transaction.

This is handled differently than operational expenses, such as the cost of filling up the gas tank in the corporate vehicle. For example, the way that this is handled is not the same. The cost of purchasing the gas tank is immediately expensed and recognised as an operational expenditure because the gas tank has a substantially shorter useful life for the company.